SK Hynix vs Micron: Which AI Memory Stock Offers Better Value in 2026?

SK Hynix is set to list on the Nasdaq on July 10, 2026, under the ticker SKHY, in what would become the largest ADR listing in history . This debut reshapes how U.S. investors evaluate AI memory stocks. For years, Micron has served as the go-to U.S.-listed proxy for trading DRAM, NAND, and AI-driven data center demand. SK Hynix, meanwhile, cemented its reputation as a dominant force in high-bandwidth memory, though its primary South Korean listing made access trickier for overseas investors. With the SKHY ADR launch, that accessibility gap is closing fast.

The real question for traders is not which company is "better." Instead, it is about identifying the superior setup: will the market reward SK Hynix for its HBM dominance and newfound liquidity, or stick with Micron's proven U.S. market access and record-breaking earnings?

Key Takeaways

- SK Hynix controls roughly 58% of the global HBM market and remains Nvidia's primary HBM supplier .

- Micron reported record Q3 FY2026 revenue of $41.46 billion, up 346% year-over-year, with gross margins exceeding 81% .

- SK Hynix trades at a valuation discount to Micron, a gap the Nasdaq listing could help close .

- Both companies face memory cycle risks, though Micron's new strategic customer agreements provide some pricing protection .

- SK Hynix and Samsung have announced $575 billion in joint spending on new facilities, which could pressure pricing by the end of the decade .

Comparing the Business Models: HBM Pure-Play vs. Diversified Memory Giant

The core distinction between these two companies boils down to this: SK Hynix leads the pure-play HBM narrative, while Micron remains the benchmark for the broader U.S. memory cycle.

SK Hynix's bullish case is anchored deeply in its high-bandwidth memory dominance. Because HBM dictates how fast data can move within AI accelerators, it acts as a critical bottleneck in the AI supply chain. This strategic importance elevates top HBM suppliers above traditional commodity memory makers. In the first quarter of 2026, SK Hynix controlled 58% of global HBM market share by revenue, with Samsung and Micron following at 21% each .

Micron casts a wider net. While it certainly has a compelling AI memory angle, it is deeply entrenched across DRAM, NAND, data center storage, PCs, and the automotive sector. Micron's appeal lies in offering a highly liquid, well-diversified vehicle to trade the broader memory upcycle. Its Q3 FY2026 results demonstrated the power of this model: $41.46 billion in revenue, up 346% year-over-year, with gross margins crossing 81% for the first time . Micron's entire 2026 HBM output is already sold out, and the company said it can fulfill only half to two-thirds of current customer demand .

Where Each Company Stands in the HBM Race

When it comes to HBM, SK Hynix still holds the edge. Its status as a primary HBM supplier to tech giants like Nvidia and Google is the main catalyst driving global interest in its U.S. listing. The company is also the first to begin testing next-generation HBM4E chips, suggesting its technological lead may persist .

However, this lead is not undisputed. Both Micron and Samsung are pouring aggressive capital into HBM development. Samsung is shifting half of its HBM production capacity to HBM4 and has halted production of 8-layer HBM3E to focus on next-generation products . Moving forward, the battle will be won on execution: HBM4 development timelines, yield rates, advanced packaging capacities, and the ability to secure long-term supply agreements.

Micron is also making strides. The company's HBM revenue grew by over 35% sequentially in Q3 FY2026 . While SK Hynix remains the leader, Micron's aggressive push into HBM suggests the competitive landscape could shift faster than many expect.

Earnings Reality Check: Micron's Record Numbers vs. SK Hynix's Momentum

Micron is not quietly taking a back seat. Its latest financial disclosures make the comparison incredibly compelling. Beyond the record revenue figures, Micron has signed 16 strategic customer agreements that lock in pricing and demand over the next three to five years. These contracts represent a minimum value of $100 billion and give Micron greater confidence in its capital expenditure plans .

These agreements are a wake-up call for the market: Micron is no longer just a cyclical recovery play. It is actively proving that AI-driven demand translates directly into massive revenue growth and margin expansion. This sets a steep benchmark for SK Hynix. Once SKHY hits the U.S. exchanges, it will have to measure up against Micron's tangible earnings horsepower rather than just its HBM narrative.

SK Hynix has also delivered remarkable earnings growth, with Q1 2026 operating profit of 37.6 trillion won and net profit of 40.3 trillion won . Year-over-year profit growth exceeded 500%, demonstrating the powerful impact of the AI memory boom. However, SK Hynix's earnings history shows more volatility than Micron's, reflecting its heavier concentration in HBM and DRAM markets.

Valuation Gap: Will the Nasdaq Listing Close the Discount?

The most compelling bull case for SK Hynix centers on valuation discount repair. SK Hynix currently trades at a lower valuation multiple than Micron. Over the past 13 years, Micron has traded at an average 35% premium to SK Hynix . The reasons have little to do with business quality: they are "better access to U.S. investors, more shareholder-friendly policies, and higher beta supported by a smaller earnings base" .

The Nasdaq listing directly addresses the accessibility factor. Eugene Asset Management and Jupiter Asset Management project up to 30% upside for SK Hynix's Seoul-listed shares over the next year if its price-earnings multiple catches up to Micron's . HSBC applied a 20% premium to its prior price-to-book estimate for SK Hynix, raising the P/B multiple from 2.8x to 3.4x, and upgraded its price target from 2.9 million won to 4.0 million won .

However, this discount may not close overnight. U.S. investors will want to see sustained earnings quality, transparent corporate governance, and consistent shareholder returns before fully embracing SK Hynix at a Micron-equivalent multiple. The listing removes the accessibility barrier, but it does not automatically eliminate the premium Micron has earned through years of U.S. market presence.

The Capacity Expansion Dilemma Facing Both Companies

Despite the bullish catalysts, a major risk looms for both companies. SK Hynix and Samsung have announced plans to spend a combined 2,000 trillion won (about $1.3 trillion) on new facilities over the next decade . A joint initiative between the two companies will build four new chip fabrication plants with a total cost of about $520 billion, plus another $53 billion for a new chip packaging facility .

SK Hynix itself aims to double its wafer capacity over the next five years . While the memory market is currently undersupplied and HBM demand is expected to grow 30% annually through 2030, the risk is that all three major players bring new factories online around 2027 or 2028, creating an oversupply that pushes prices down across the industry .

Micron's strategic customer agreements provide some protection. Those contracts guarantee a minimum of $100 billion in revenue and include pricing floors for about 20% of DRAM volume and one-third of NAND volume . But if industry-wide oversupply becomes severe enough, even contracted pricing could come under pressure. Micron's Q3 FY2026 results showed it was able to sell all of its HBM capacity and still turn away customers, but that dynamic could reverse once new factories begin production .

SK Hynix Stock Price Prediction 2026

Analysts remain broadly constructive on SK Hynix's outlook. The average price target for the Korean shares is approximately 3.09 million won, with 35 of 37 analysts rating it a Buy . UBS has raised its target to 3.2 million won, citing long-term agreements locking in 60-70% of expected volume and pricing .

The bull case assumes the Nasdaq listing closes the valuation gap with Micron, HBM demand remains strong, and memory pricing continues improving. UBS forecasts DRAM average selling prices to rise 43% quarter-over-quarter in Q2 2026, with further increases in the second half. Operating profit for Q2 2026 is projected at approximately 69 trillion won .

The bear case would involve HBM demand slowing, memory pricing weakening, or the massive capacity expansion leading to oversupply sooner than expected. SK Hynix shares have already shown volatility, dropping more than 17% in July 2026 before rebounding, reflecting these competing narratives. The ADR offering itself creates near-term dilution risk, as the company is issuing approximately 17.79 million new shares .

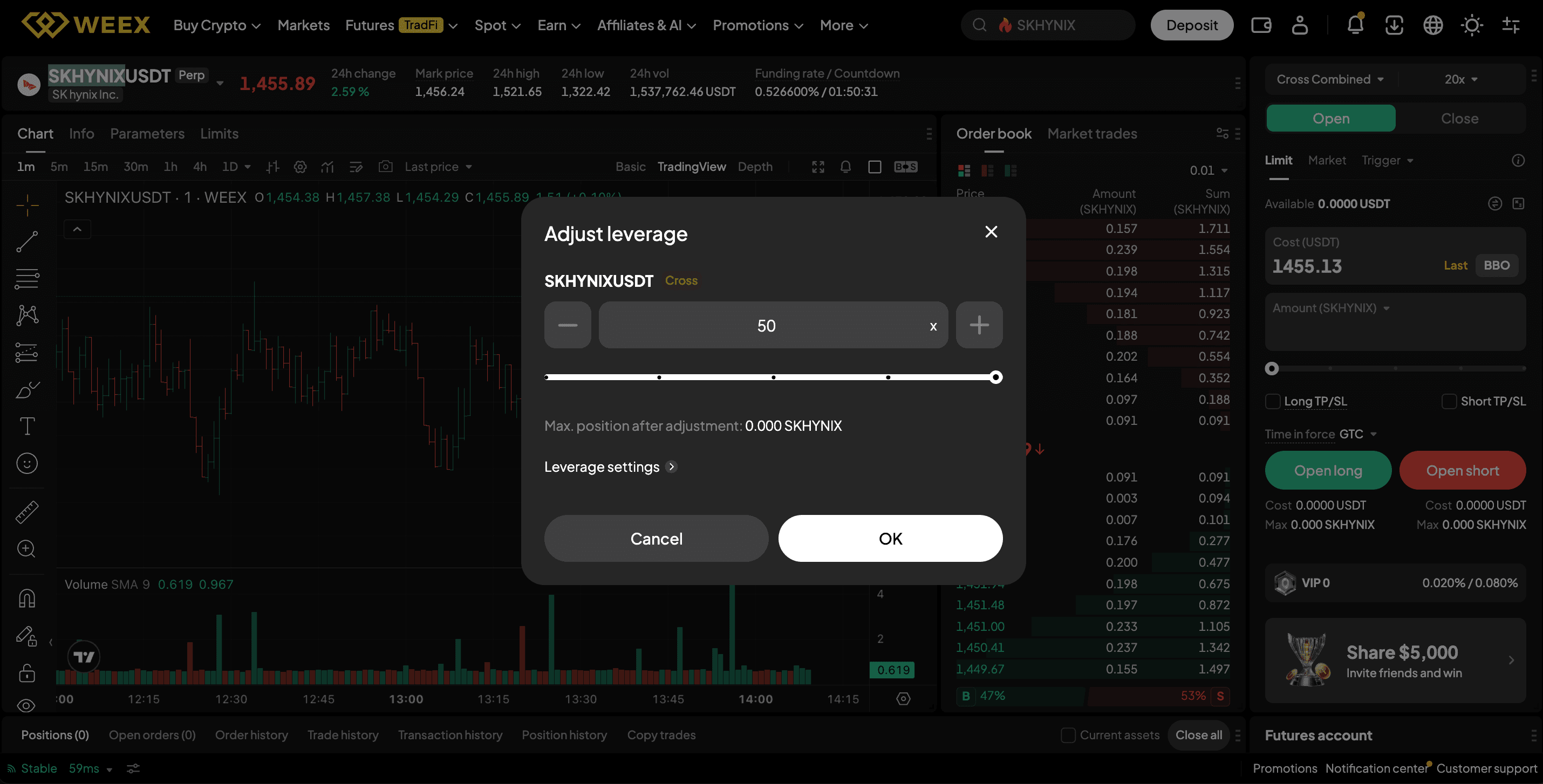

How to Trade SK Hynix and Micron Stock

WEEX users can access both SK Hynix and Micron exposure through the TradeFi market. Here are the steps to trade SK Hynix and Micron on WEEX:

Step 1: Go to WEEX official website and create your account.

Step 2: Fund your account. Transfer USDT to your account or buy crypto directly using fiat or quick buy.

Step 3: Navigate to the futures section and search for SKHYNIXUSDT trading pair.

Step 4: Choose to go long or short. WEEX supports up to 400x leverage.

Step 5: Set take profit(TP) or stop loss(SL).

Step 6: Monitor your order.

Conclusion

SK Hynix and Micron both offer compelling exposure to the AI memory trade, but they serve different investment theses. SK Hynix provides concentrated exposure to HBM leadership and a potential valuation re-rating from the Nasdaq listing. Micron offers diversified memory exposure, deep U.S. liquidity, and earnings transparency backed by strategic customer agreements.

The choice depends on an investor's risk tolerance and time horizon. Short-term traders may find opportunity in SK Hynix's Nasdaq debut momentum and potential index inclusion. Long-term investors should weigh the capacity expansion risks and whether SK Hynix can maintain its HBM lead against Samsung's aggressive push. Both stocks have delivered exceptional returns over the past year, and both face the fundamental risk that memory remains a cyclical business.

FAQ

1: Is SK Hynix better than Micron for AI memory exposure?

SK Hynix currently commands the stronger HBM leadership narrative with roughly 58% market share. Micron offers a more diversified memory business with established U.S. liquidity.

2: Why is SK Hynix's Nasdaq listing important for investors?

The Nasdaq listing removes a long-standing accessibility barrier for U.S. investors. The listing could close this valuation gap.

3: Which company is more exposed to HBM?

SK Hynix has the stronger pure-play HBM exposure. While Micron is expanding its HBM footprint, its overall business remains more diversified across DRAM, NAND, and enterprise storage.

4: What is the biggest risk for SK Hynix after the listing?

The biggest risks are the massive capacity expansion plans by SK Hynix and Samsung, which could lead to oversupply and pricing pressure by 2027-202 .

5: What is the biggest risk for Micron?

The biggest risk is that the massive capacity build-out by SK Hynix and Samsung undermines Micron's pricing power despite its strategic customer agreements.

Disclaimer: For informational purposes only. Not financial advice. Any activities, rewards, campaigns, or promotions mentioned do not constitute an offer, solicitation, or recommendation to buy, sell, or trade crypto assets. Crypto assets are highly volatile and may lose value. WEEX services, products, or campaigns may not be available in all regions. Users are responsible for complying with applicable local laws before participating.